Table of Content

Unsecured loans have many advantages — the biggest being that you don’t risk losing a valuable personal asset if you can’t repay the loan. These loans tend to have a simple application process and give you fast, flexible use of funds. There are some drawbacks, though, such as tougher eligibility requirements and higher interest rates than secured loans. Some unsecured loans are designed specifically for borrowers with bad credit.

Adding luxury items at home can exponentially increase the worth of your home. Homeowners with this personal loan option can also borrow a loan for adding luxury items too. Get personalized pre-qualified offers with no impact to your credit score. A secured loan is secured by collateral, which can either be a motor vehicle, house, savings account, certificate of deposit, etc. For example, a home equity line of credit average interest rate is currently in the ballpark of 4% for a $50,000 loan with an 80% loan-to-value ratio. Debt CollectorsA debt collector is a person or company hired by a business to track and recover debt owed on sales of goods and services that exceed accepted payment terms.

About TGUC Financial

No, checking your pre-approved offer or loan eligibility will not affect your credit score. From a home renovation project to consolidating your debt, managing a medical emergency, to wedding expenses, you can use your loan amount for almost any planned or unplanned expense. In a home equity line of credit, the interest rates will fluctuate and it is determined by your credit score.

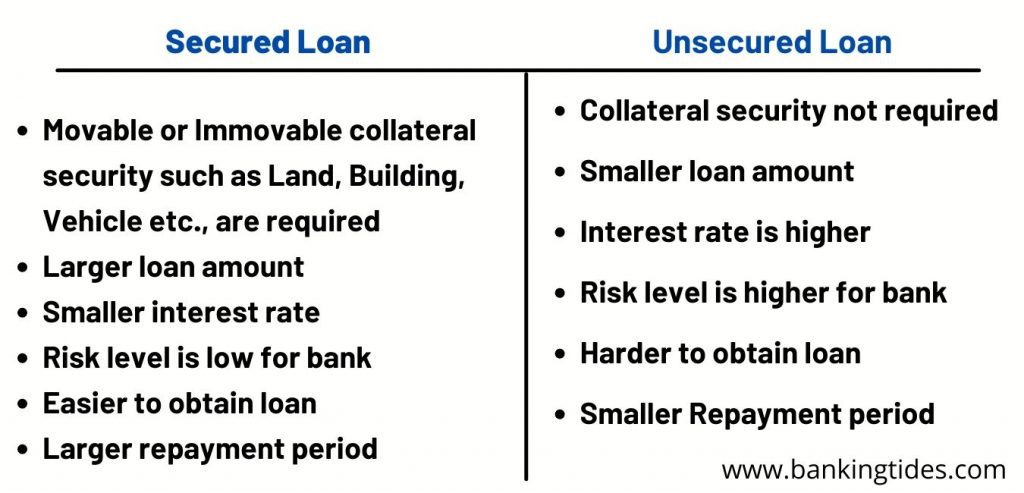

A secured loan requires that the borrower take a portion of his or his or her property as collateral. In the event of default the lender could purchase the collateral and then sell it in order to get the money back. In the end, the interest rate on these loans is less than that of loans with no collateral. However, they can be accompanied by high arrangements fees and other costs. If you do have the right to qualify, the amount you’re able to borrow will depend on the worth of your home.

Personal Loans

When you take out a secured loan, the lender puts a lien on the asset you offer up as collateral. Once the loan is paid off, the lender removes the lien, and you own both assets free and clear. Your credit score is one of the most critical elements when it comes to your personal loan approval. Bajaj Finserv offers a free CIBIL score check to help you ascertain your credit score.

Before you can apply for one, it is important to be aware of what you want to achieve and how much you’ll need and what kind of credit you’ve earned. This will allow you to find the most suitable loan for your requirements. If you’re a bad credit holder and are unable to repay your loan, unsecured loans may not be the best option for you. Secured loans are ideal for people with less than perfect credit since lenders provide extra protection in the event that you fail to repay the loan. When planning to take out a personal loan, a borrower can choose between secured vs unsecured loans. When borrowing money from a bank, credit union, or other financial institution, an individual is essentially taking a loan.

Online account

If you can’t resolve the issue with your lender, your lender can start the process of taking your assets to prevent their losses. The purpose of this question submission tool is to provide general education on credit reporting. However, if your question is of interest to a wide audience of consumers, the Experian team may include it in a future post and may also share responses in its social media outreach.

She has expertise in finance, investing, real estate, and world history. Kirsten is also the founder and director of Your Best Edit; find her on LinkedIn and Facebook. Christina Majaski writes and edits finance, credit cards, and travel content.

Unsecured vs. Secured Debts: An Overview

A secured loan is a type of loan where the lender requires the borrower to put up certain assets as a surety for the loan. In most cases, the asset pledged is usually tied to the type of loan that the borrower has applied. For example, if the borrower has requested for an auto loan, the collateral for the loan would be the motor vehicle to be financed using the loan amount. There are many credit institutions, banks, and online companies offering them. A borrower should compare the rates across different institutions and ensure that the repayment can happen timely to avoid attracting legal action.

Most lenders have their own set qualifications such as a minimum credit score or a minimum annual income. If you do not meet these standards, you can still possibly obtain a loan through that lender by using a cosigner or co-borrower. In other cases, you can secure financing but at a higher than average interest rate.

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. If you’re in the market for a mortgage, check interest rates often to stay up-to-date on rate trends.

If you have bad credit and you’re willing to pay more for a home improvement loan, consider applying for a home improvement loan for bad credit. Some lenders might approve you for a loan with a credit score as low as 580. Having a longer repayment term might be better for your budget since your monthly payments could be lower. However, the downside to this is that you’ll end up paying more in interest during the life of the loan.

If the homebuyer defaults on an unsecured loan, the lender cannot claim rights to the property. The advantage of a unsecured home loan is that, even though the lender may sue if payments are not made, the buyers run less risk of losing their home if they default. However, getting this mystical, magical unsecured loan is a difficult process. To begin with, the underwriting standard for an unsecured loan is far more detailed than for a normal loan.

The risk of default on a secured debt, called the counterparty risk to the lender, tends to be relatively low. It could take some time to save up enough to pay for home improvements. The upside is you can complete projects without racking up debt and having to repay lenders for years to come. To illustrate, if you get a 10-year home improvement loan for $50,000 with a fixed rate of 8 percent, you’ll pay $607 each month and $22,796.56 in interest over the loan term. But if the term is extended to 30 years, your payment will drop to $367, but you’ll pay $82,077.62 in interest. Information provided on Forbes Advisor is for educational purposes only.

It’s also important to note that unsecured loans do not carry the risk of secured forms of financing such as home equity loans which put your personal assets at risk. Since unsecured loans are more risky for lenders, they usually come with lower maximum loan amounts. Depending on your financial situation, most lenders might allow you to borrow up to $50,000, and a few lenders might let you borrow up to $100,000 if you have a large income. Still, the loan amount may not be sufficient to cover the costs of the home improvements you have in mind. Once your finances are in order, start shopping for lenders that offer the most competitive APRs and flexible repayment terms.

Fill out a form online to pre-qualify with no impact to your credit score. Companies displayed may pay us to be Authorized or when you click a link, call a number or fill a form on our site. Our content is intended to be used for general information purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances and consult with your own investment, financial, tax and legal advisers.

No comments:

Post a Comment